By Alberto Onetti

The rise of dual-use technologies — innovations with both civilian and military applications — is rapidly transforming the global tech landscape. Once a niche, largely avoided due to LP restrictions on defense-related investments, the category is now front and center for governments, VCs and startups alike.

The drivers are clear: Intensifying geopolitical tensions, ballooning defense budgets across NATO countries, and a growing awareness that critical future capabilities — from AI-driven surveillance to autonomous systems and secure communications — will increasingly originate not just from traditional defense contractors, but from agile, high-growth startups.

How big is dual-use tech? How much is defense?

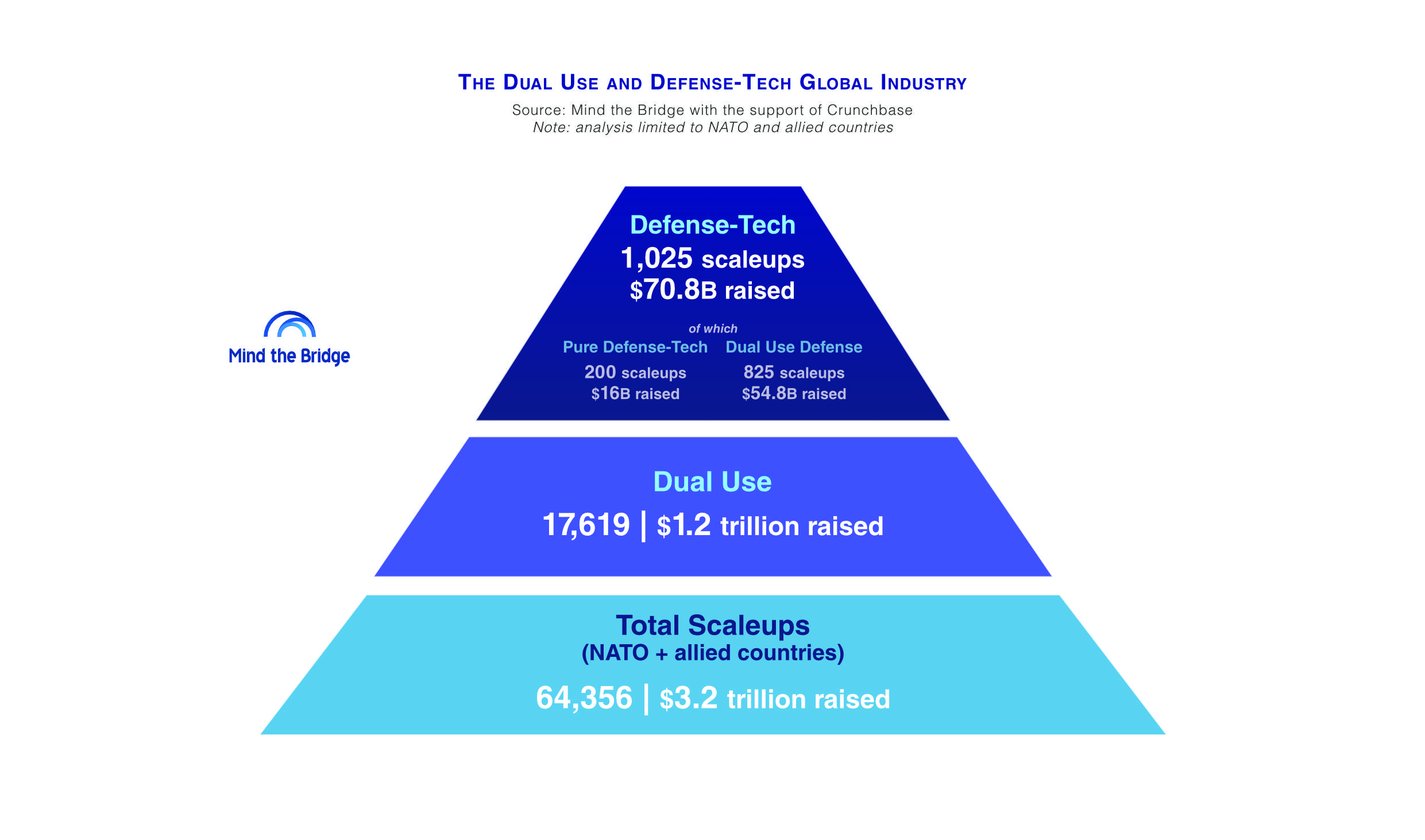

As of May 2025, there are 17,619 dual-use tech scaleups operating across NATO countries — out of a total of approximately 64,000 scaleups identified in the 47 countries analyzed.

Within this cohort:

1,025 are categorized as defense tech scaleups.

Of these, 200 are “pure defense tech,” or startups focused exclusively on military applications.

The remaining 825 are “dual-use defense tech” — startups that began with civilian technologies and later evolved to include defense-oriented solutions.

Put differently, dual-use tech scaleups now make up 27% of the total scaleup population in the countries examined. That’s 1 in every 4 scaleups developing technologies with potential military or defense applications.

The surge of dual-use technologies

This is no longer a trend — it’s a surge. Powered by Fincantieri, Mind the Bridge and Crunchbase conducted a first analysis in late 2024 (report here). Midway through 2025, we updated it (download here) to reflect the latest developments.

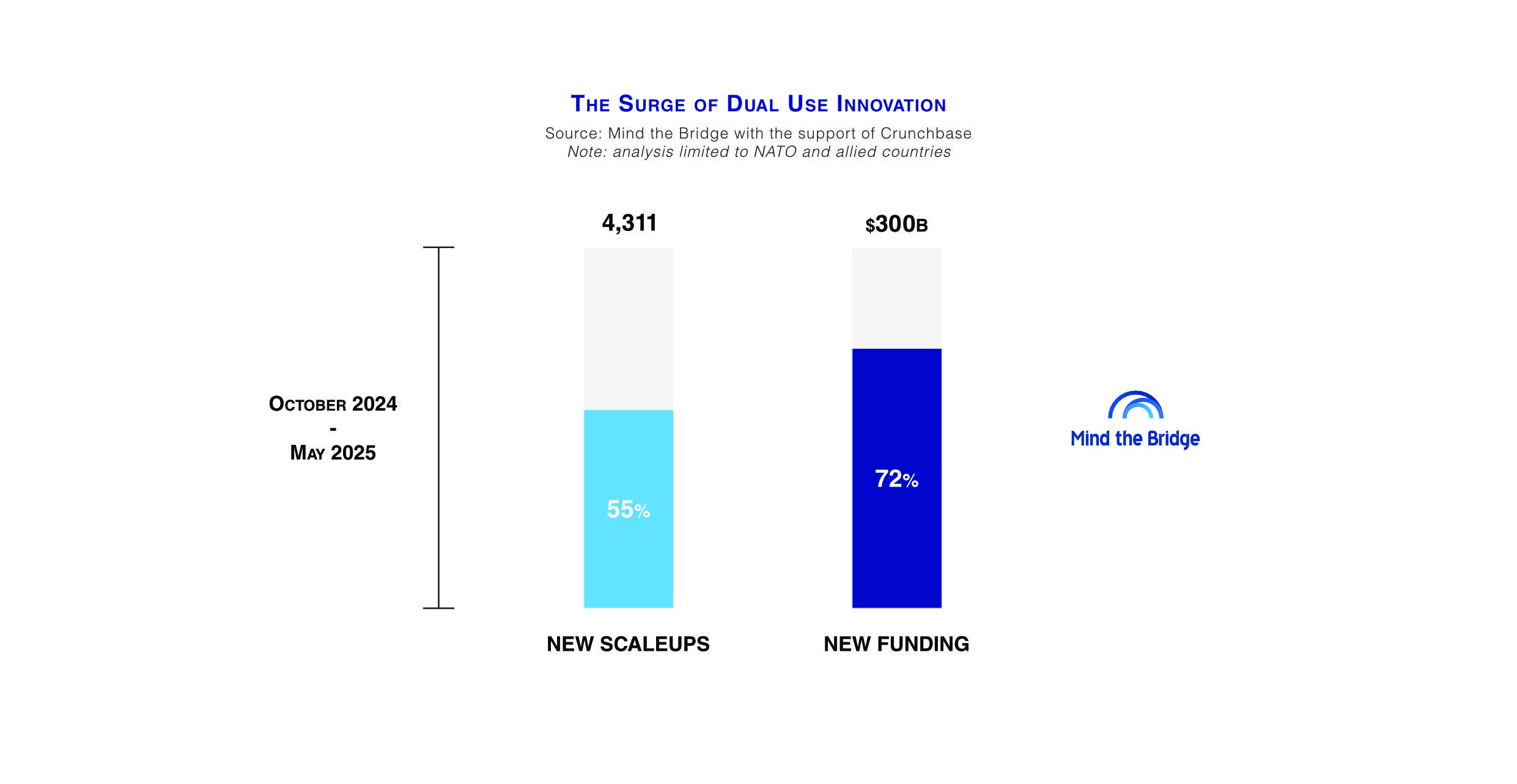

What we found is that in just six to eight months, growth has been nothing short of explosive.

The number of dual-use tech scaleups rose from 15,260 to 17,619, a 16% increase.

Defense tech scaleups crossed the 1,000 mark (up 13%), with pure defense tech growing even faster at a rate of 18%-plus.

Investment in dual-use tech skyrocketed 25%, from $954.5 billion in Q3 2024 to nearly $1.2 trillion in May 2025.

Defense tech-specific investment jumped 27%, reaching $70.8 billion.

Between October 2024 and May 2025 alone:

4,311 new scaleups were created across NATO and allied countries.

More than half (2,359) are dual-use tech companies.

Roughly 70% of all new scaleup investment during this period went to dual-use tech startups.

Where dual-use tech is more advanced

Israel pioneered the model, converting military R&D into a startup-driven tech powerhouse. The U.S. follows with a growing network of integration programs (DIU, AFWERX, NSIN) to onboard commercial innovation into the defense ecosystem.

Europe is catching up. In 2024 alone, the EU committed €1.5 billion to defense-related R&D via initiatives like EDIRPA and the European Defence Fund. Meanwhile, national programs are expanding:

The U.K. pledged £400 million for defense innovation;

Germany doubled its military procurement budget; and

NATO’s €1 billion Innovation Fund has begun backing dual-use startups across the alliance.

Even smaller, digitally advanced countries are moving quickly. Estonia stands out for integrating its startup ecosystem into national defense strategy. But it’s not alone: Ukraine, Poland, Czechia and other Eastern European countries are also investing heavily in defense innovation.

Barriers do exist

Despite this momentum, dual-use innovation still faces serious challenges. These startups develop hard tech with critical military applications — often requiring long R&D cycles and large funding rounds.

Our data shows that defense tech startups are more capital-intensive. Pure defense tech scaleups have raised an average of $80 million. That compares with $66 million on average for dual-use tech and $50 million for purely civilian tech scaleups.

They also face longer time-to-market, due to procurement bottlenecks and outdated acquisition models. This creates a notorious “Valley of Death” post-pilot phase.

Common barriers include:

Startup fragility raises real concerns about survivability;

Many armed forces are unaccustomed to working with TRL 6-stage startups; and

Scaling and field deployment remain major bottlenecks. Defense startups can’t go it alone. Most lack the infrastructure to scale hardware production.

Moreover, dual-use startups often suffer from a “not here nor there” syndrome — torn between two demanding markets, without fully committing to either. This can dilute strategic focus and stall growth.

Fundraising and exit opportunities are another friction point:

Many institutional LPs remain hesitant or hindered to back defense-related ventures.

Exit options are limited. National security restrictions often block foreign M&A, while local buyers are few and far between.

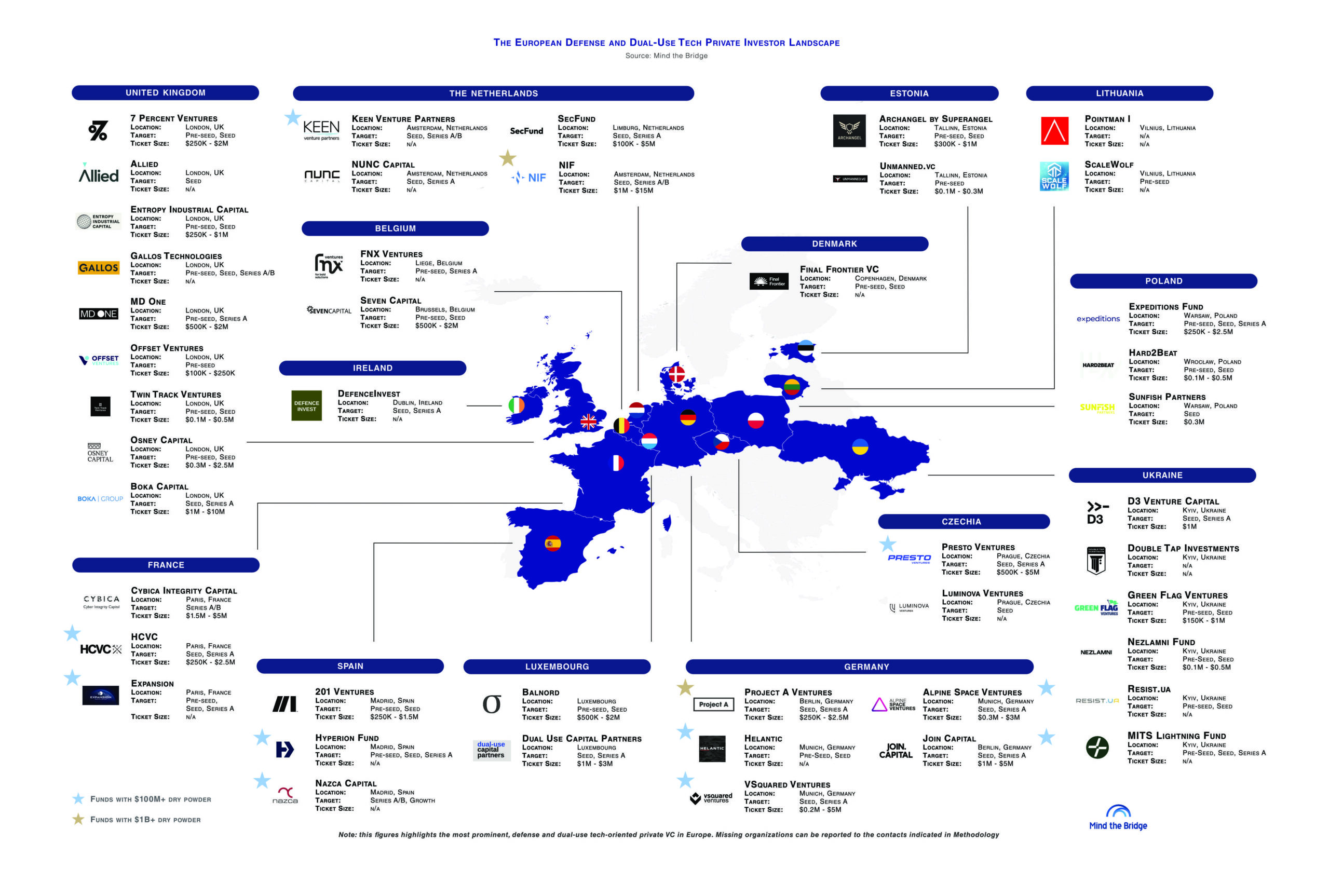

That said, the landscape is shifting. Mind the Bridge identified 74 VC funds globally that actively invest in dual-use startups. More than one third (35%) are based in the United States, followed by the U.K. (12%). Another 22% are located in Ukraine, the Baltics and Eastern Europe — a sign of the growing relevance of defense and security tech in these regions. (A searchable global directory of investors active in dual-use is available here.)

Alberto Onetti is chairman of Mind the Bridge and a professor at University of Insubria. He is a serial entrepreneur who has started three startups in his career, the last of which is Funambol, among the five Italian scaleups that have raised the largest amount of capital. He is recognized among the leading international experts in open innovation and has wide experience in setting up and managing open innovation projects — venture clients, venture builders, intrapreneurship, CVCs — with large multinational companies, as well as advising and training on this subject. Onetti has a column on Sifted (Financial Times) and several other tech blogs.

Illustration: Dom Guzman

Stay up to date with recent funding rounds, acquisitions, and more with the

Crunchbase Daily.