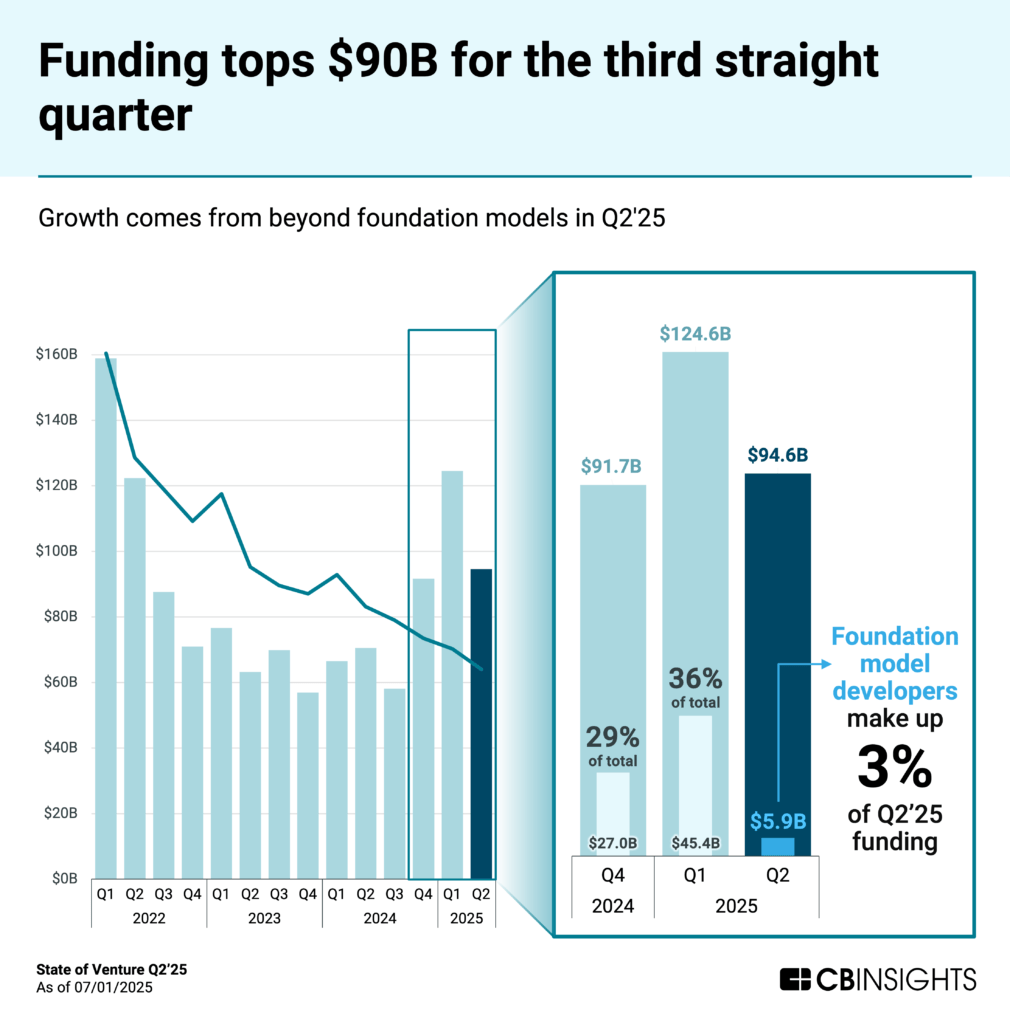

Venture funding surpassed $90B for the third consecutive quarter in Q2’25, even as deals slid to their lowest levels since Q4’16.

AI continues to dominate, capturing 50% of venture investment. At the same time, investors are doubling down on hard tech — hardware-focused and capital-intensive technology — driven by surging energy demands from AI, advancements in robotics, and growing defense interest.

Below, we break down the top stories from this quarter’s report, including:

Funding tops $90B for the third straight quarter, while deal count declines

Hard tech claims 6 of the top 10 largest deals

AI companies command funding premiums across sectors

Regulatory shifts push big tech from M&A to minority investments

CVC deals hit a 7-year low as the tariff threat looms

We also outline the categories shaping venture dealmaking for the rest of 2025 — including stablecoins, defense tech, quantum, and nuclear energy.

Let’s dive in.

Download the full report to access comprehensive data and charts on the evolving state of venture across sectors, geographies, and more.

Top stories in Q1’25

1. Funding tops $90B for the third straight quarter, while deal count declines

Venture funding reached $94.6B in Q2’25, marking the second-highest quarterly figure since Q2’22 and the third straight quarter to surpass $90B.

While funding dipped slightly from Q1’25, the decline reflects normalization after OpenAI’s $40B raise inflated numbers in Q1. In fact, Q2 remained elevated even as foundation model developers accounted for just 3% of total capital, down from 36% in Q1’25 and 29% in Q4’24. This shift signals a broadening of venture activity beyond foundation models into the broader AI ecosystem and adjacent hard tech sectors.

With this continued momentum, annual funding is projected to reach nearly $440B, a 53% increase from 2024, pointing to a sustained recovery in venture investment.

At the same time, deal volume continues to decline, reflecting greater investor selectivity. Q2 saw just 6,028 deals — the lowest quarterly total since Q4’16. This puts 2025 on pace for around 25,000 deals, or nearly half the volume seen in 2022, even as total funding approaches similar levels.

While investors are pulling back on the number of deals, they’re deploying more capital per investment: the median deal size hit a new high of $3.5M in 2025 YTD. Rising check sizes and falling deal count underscore a shift toward fewer, higher-conviction bets.

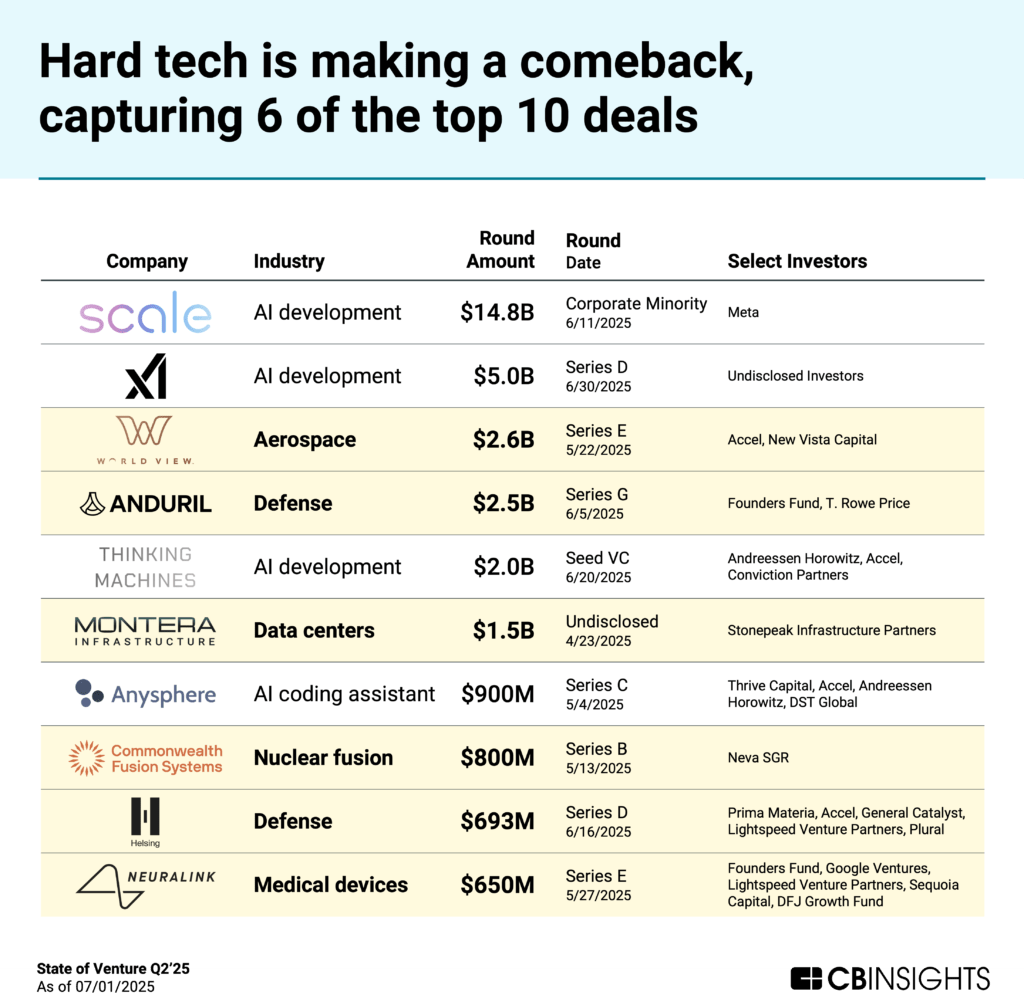

2. Hard tech claims 6 of the top 10 largest deals

Six of the 10 largest deals in Q2’25 went to hard tech companies, which are firms building capital-intensive physical products.

This surge is driven by macro forces such as onshoring initiatives, clean energy investment, and the rise of physical AI, which is enabling new capabilities across robotics, autonomy, and industrial systems.

Mega-rounds ($100M+ deals) spanned multiple sectors:

Geopolitical tensions are also pushing capital toward defense, where startups are securing large rounds:

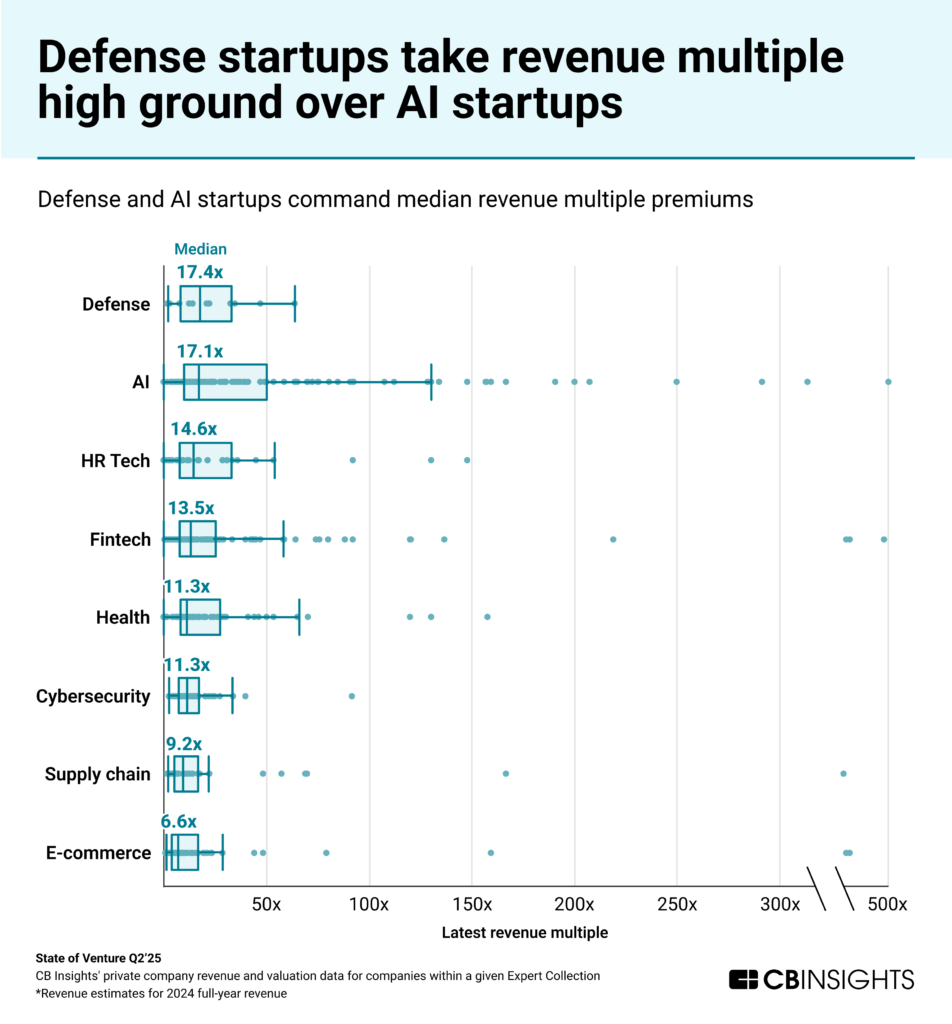

Across the board, defense tech startups are now commanding a median revenue multiple of 17.4x, edging out AI companies at 17.1x and all other major sectors. This signals high investor confidence and competition, driving premium valuations across the defense tech sector.

With investor appetite moving toward physical infrastructure and embodied AI, the rise of hard tech represents a shift likely to define the next chapter of venture investing.

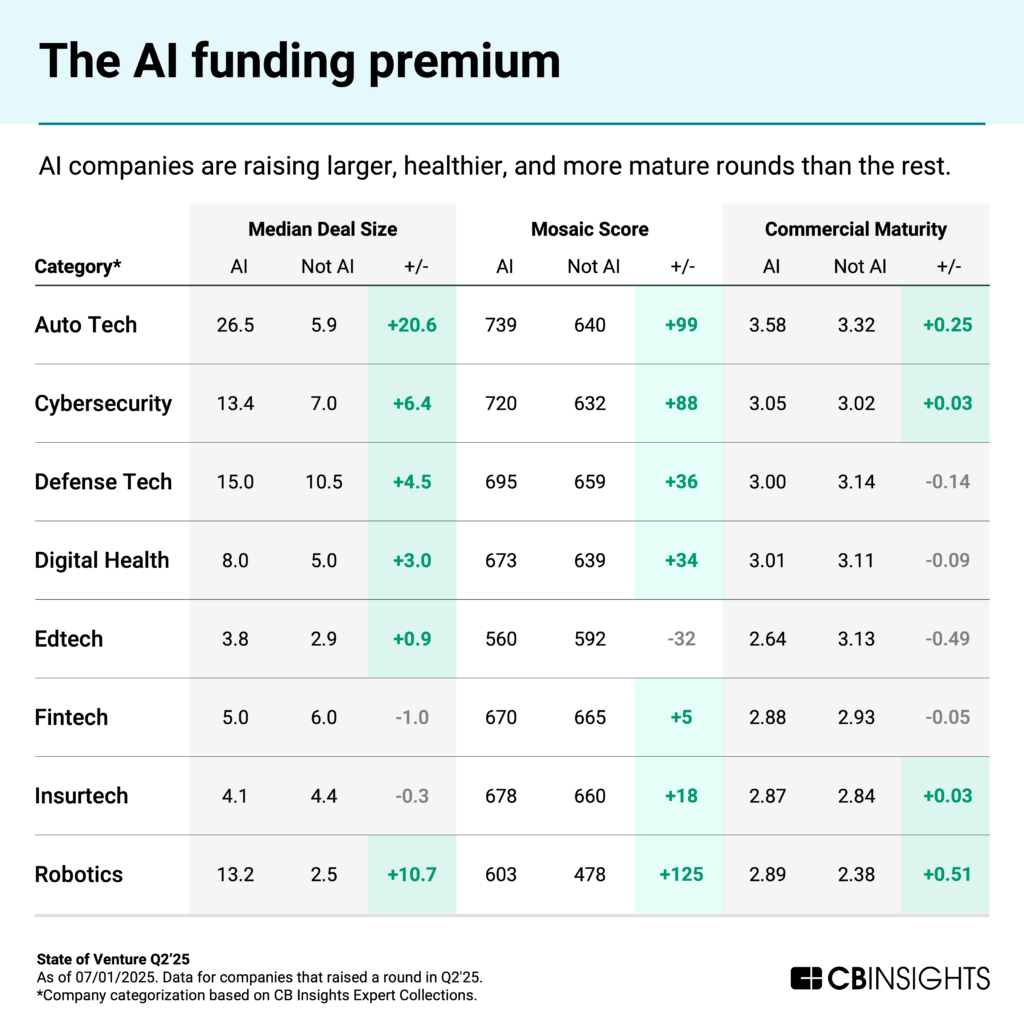

3. AI companies command funding premiums across sectors

The venture market is experiencing a pronounced “AI premium,” with median deal size for AI companies reaching $4.6M in 2025 — over $1M more than the broader market.

But the premium isn’t just financial. AI companies also score higher on CB Insights’ Mosaic Score (success probability) and Commercial Maturity (ability to compete and partner) across most sectors, signaling stronger fundamentals and market readiness in the eyes of investors.

AI companies in auto tech — with most focused on autonomous driving — are commanding the highest premium. Their median deal size is $20.6M higher than non-AI auto tech peers, and their average Mosaic score is 99 points greater. This quarter, the largest AI auto tech deal went to Applied Intuition, which raised a $600M Series F round at a $15B valuation.

Robotics and cybersecurity follow closely, with AI firms in those sectors securing median deal sizes $10.7M and $6.4M larger than their non-AI peers.

Team pedigree is further amplifying the premium. Thinking Machines Lab — founded by former OpenAI CTO Mira Murati alongside veterans from OpenAI, Google, Meta, and Mistral AI — raised a record-breaking $2B seed round at a $10B valuation, making it the most valuable seed-stage startup ever.

The deal reflects an increasingly common “go big or go home” investing mentality, as investors make outsized bets on high-credibility AI teams.

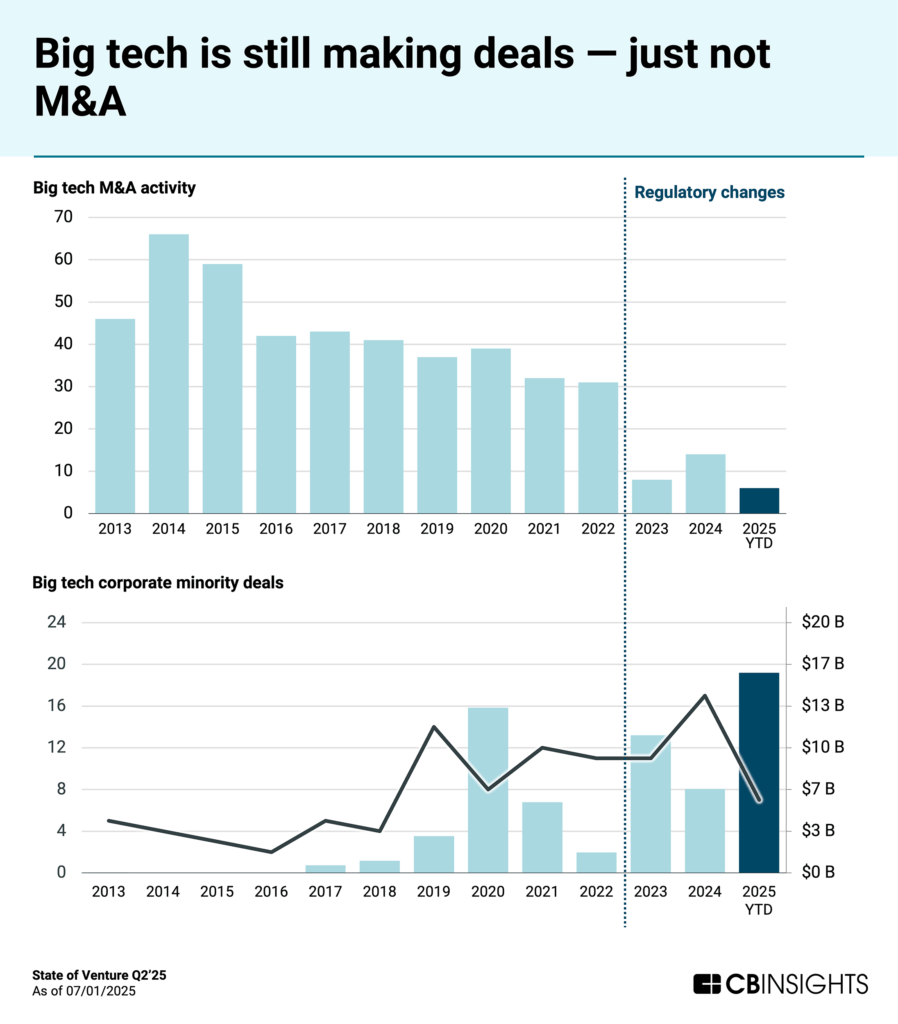

4. Regulatory shifts push big tech from M&A to minority investments

Big tech M&A — which includes M&A from Alphabet, Amazon, Apple, Microsoft, Meta, and Nvidia — is entering a sustained downturn. Annual deal activity is projected to hit just 12 transactions in 2025, a steady decline from 66 deals in 2014.

US regulatory tightening caused M&A activity to collapse from 30+ deals in 2022 to just 8 deals in 2023 — the steepest single-year decline on record.

Big tech companies are adapting by taking large minority stakes, allowing them to circumvent federal antitrust review while still gaining strategic influence and access to key technologies. For example, Meta invested $14.8B in Scale — the largest funding round of Q2’25 — for a 49% stake, as did Microsoft with its recent investments in OpenAI.

In 2025 YTD, big tech is on pace for 14 corporate minority deals, an increase from levels before the regulatory shift.

Big tech’s shift reflects broader M&A weakness across the market. Global activity has fallen 34% from 3,103 deals in Q1’22 to 2,053 deals in Q2’25, driven by high interest rates that have made financing more expensive and economic uncertainty that has made companies more cautious about acquisitions.

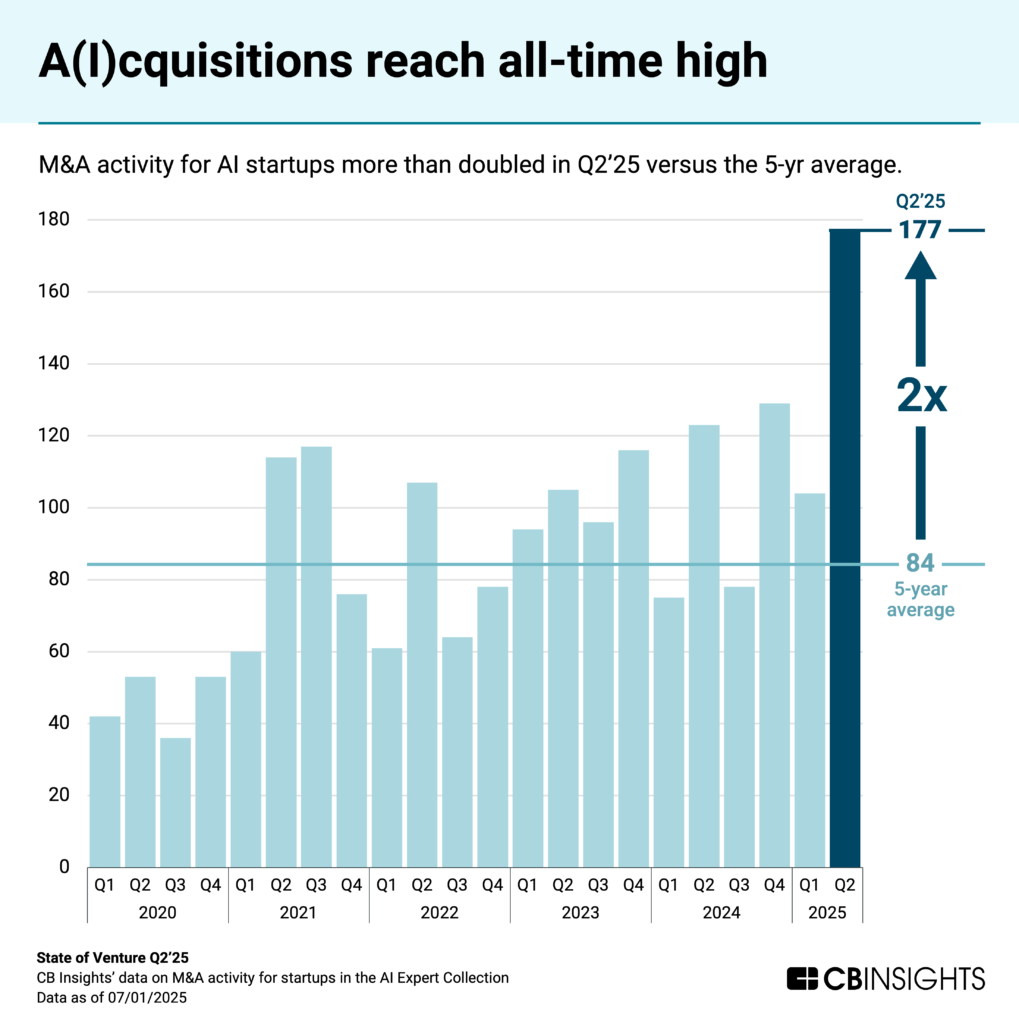

However, acquisitions of AI companies is one area where M&A is increasing. Activity reached record levels in Q2’25 at 177 deals — over double the 5-year quarterly average of 84 deals. This surge reflects companies’ need to acquire AI capabilities quickly rather than build them internally, as AI becomes essential for staying competitive.

While falling interest rates will help smaller deals rebound and provide a modest tailwind to overall M&A activity, we do not expect deal volumes to approach peak years. Big tech and other large corporations will remain constrained by regulatory scrutiny.

We are likely entering a new era where strategic partnerships and minority investments replace traditional M&A as a growth mechanism for major corporations.

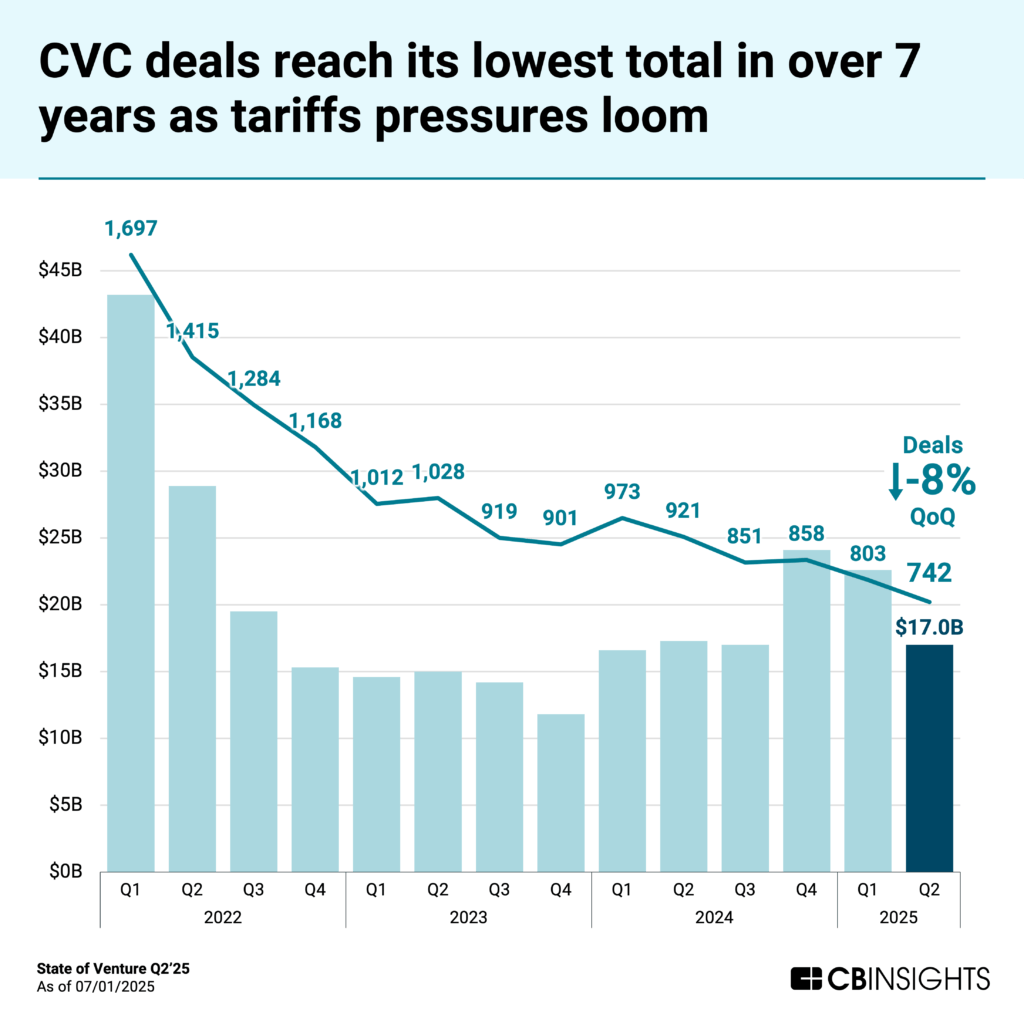

5. CVC deals hit a 7-year low as the tariff threat looms

Corporate venture capital dealmaking has reached its lowest point in over 7 years, as CVC-backed investment totaled just $17B across 742 deals, down 8% quarter-over-quarter and representing the weakest performance since Q1’18.

CVC activity has fallen dramatically from its Q1’22 peak due to broader market pressures, including high interest rates and economic uncertainty. Tariff concerns are likely adding further burden to an already weakened market.

Despite fewer deals, median CVC-backed deal sizes have reached their highest levels since 2021. This suggests that CVCs are concentrating capital on fewer, higher-conviction investments.

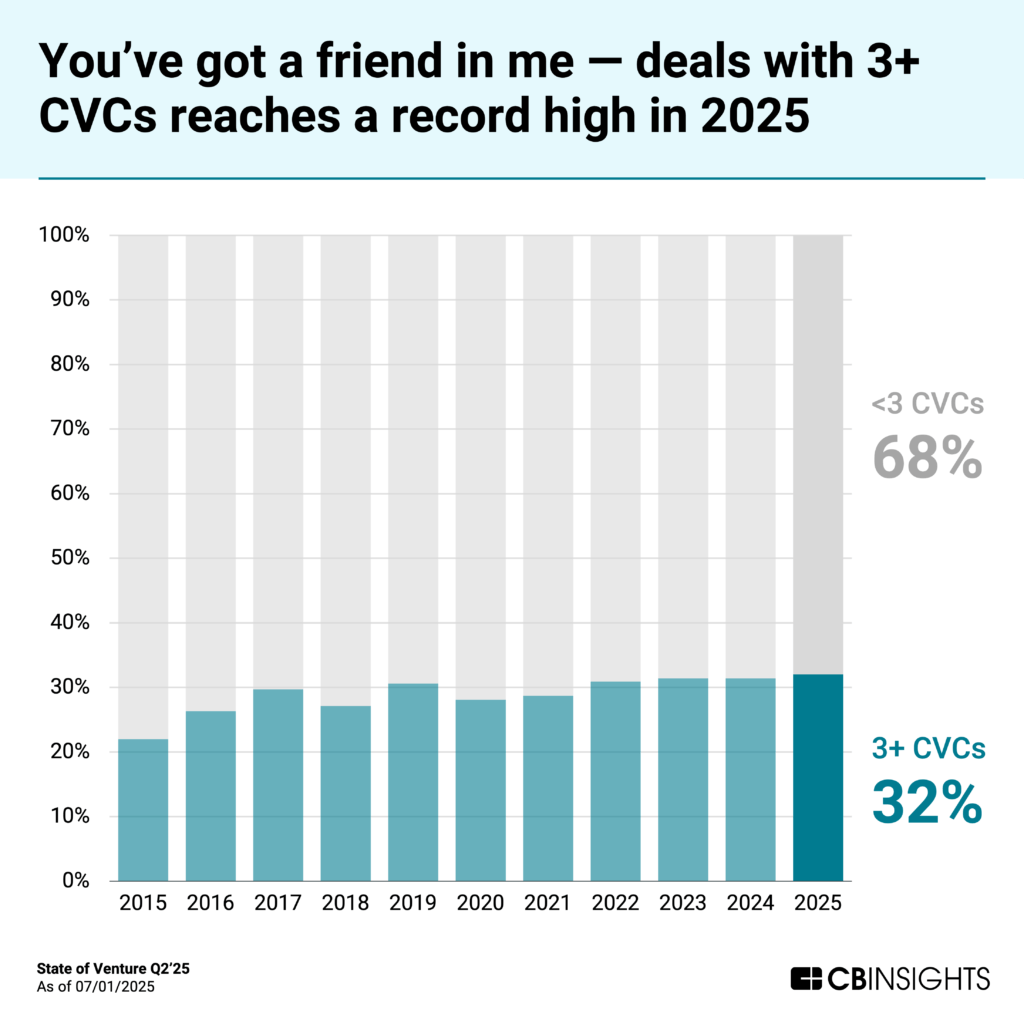

CVCs are also collaborating more frequently. Deals involving 3+ CVCs reached a record high of 32% in Q2’25, reflecting both strategic necessity and market conditions: larger funding rounds in capital-intensive sectors like AI and hard tech may require multiple corporate partners to provide sufficient capital. At the same time, competition for access to the hottest technologies drives CVCs to team up rather than risk being shut out.

Breakout sectors of 2025

Below, we analyze venture funding across tech sectors to identify where investor conviction and market momentum are strongest.

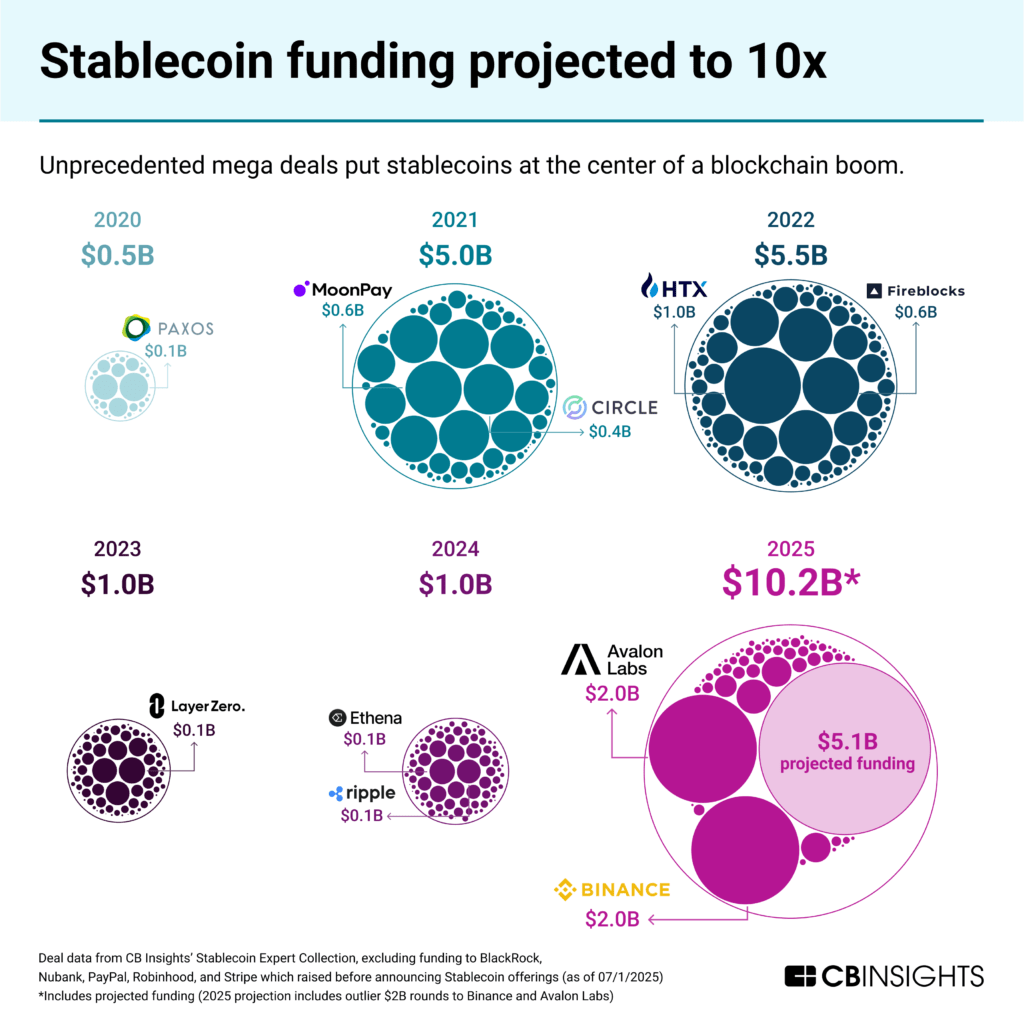

Stablecoin funding is on pace to shatter its previous record

Stablecoin startups are experiencing an explosive year-over-year funding surge as stablecoins achieve mainstream adoption. Funding is projected to reach $10.2B in 2025, representing more than 10x growth from 2024.

Growing regulatory frameworks worldwide — such as the pending passage of stablecoin legislation in the US with bipartisan support — provide needed certainty for institutional investment, setting the foundation for exponential growth.

Multiple startups are taking advantage of the momentum. While the largest funding rounds occurred during the first quarter — with $2B deals for Avalon Labs and Binance — notable rounds also occurred during Q2’25, including:

Flowdesk: $100M for digital asset trading and liquidity services

Conduit: $36M for its cross-border business transactions platform

Niural: $31M for an AI-enabled stablecoin and fiat payroll platform

Major financial services companies are also increasingly involved. Mastercard, Visa, and established banks are now enabling stablecoin transactions and issuing their own digital currencies, bringing institutional credibility to the space. Meanwhile, stablecoin issuers Circle and Ripple applied for banking licenses on June 30 and July 2, respectively, demonstrating their intent to operate like mainstream financial institutions.

Stablecoins are evolving beyond simple stores of value into yield-bearing tools and liquidity products. Solutions like liquidity mining, lending services, and yield-bearing stablecoins are receiving substantial investor attention. Cross-border payments companies powered by stablecoins are also gaining traction as affordable and accessible USD alternatives in emerging markets.

As regulatory frameworks solidify and institutional adoption accelerates, stablecoin companies are positioned to capture significant market share in global payments and financial infrastructure markets.

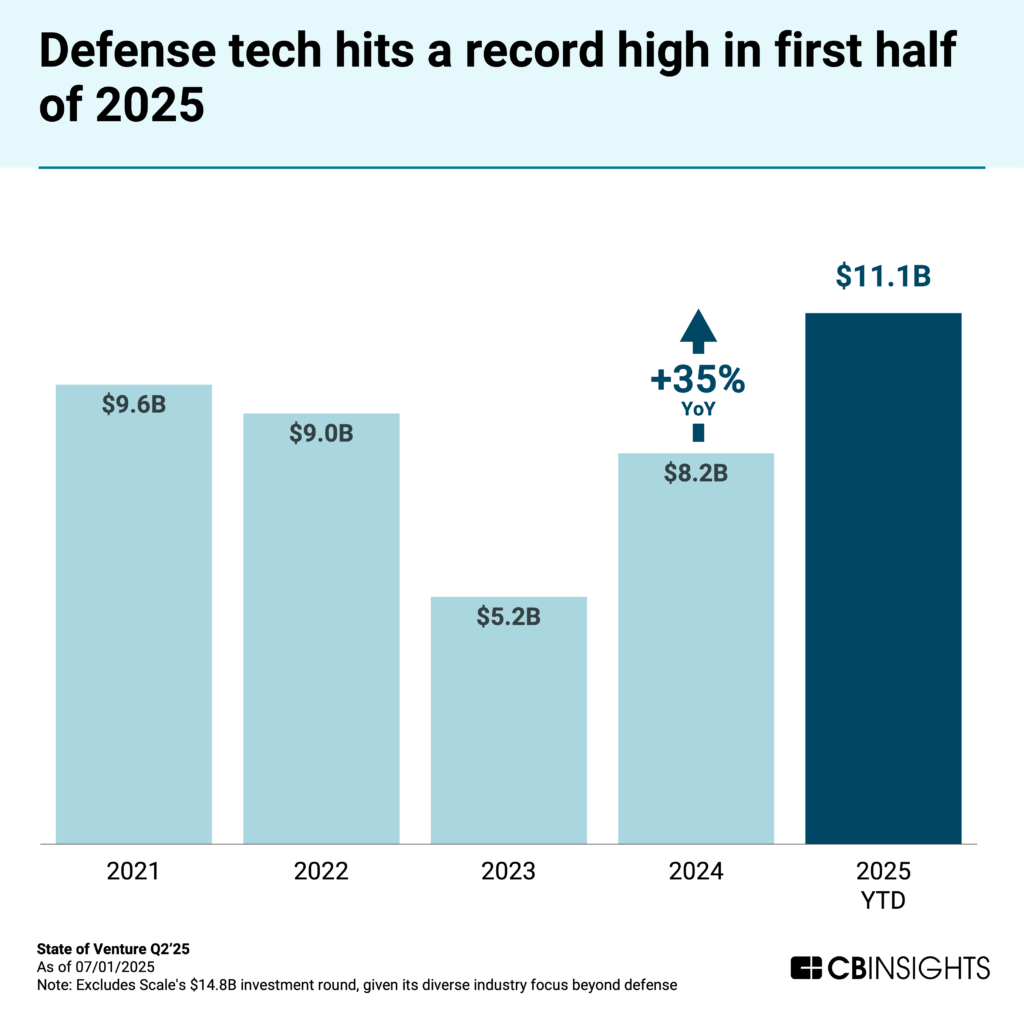

Defense tech momentum continues

Within the first two quarters of 2025, defense tech funding has already reached a new annual record of $11.1B.

The funding breakout is driven by multiple forces, including geopolitical instability and technology advancements, notably in drones and other unmanned vehicles.

Concurrently, the US Department of Defense is pushing to diversify the defense ecosystem through public-private partnerships and startup support.

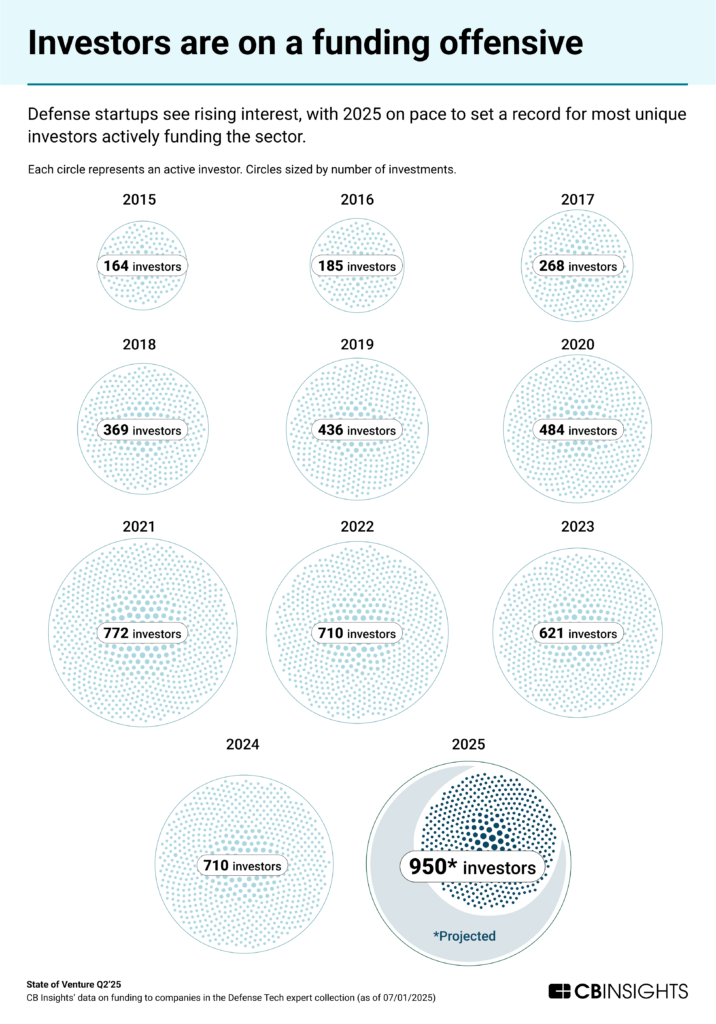

The defense investor landscape is also rapidly evolving, with the number of unique investors in the space expected to increase 34% in 2025 to 950 from 710 the year prior. Traditional defense funds like Shield Capital and In-Q-Tel are now joined by generalist VCs, bringing more capital to fund a new generation of startups.

We expect continued investor interest in defense tech, as NATO recently agreed to increase defense spending from 2% to 5% of GDP by 2035, adding over $400B annually in market expansion. The 1.5% earmarked for security infrastructure aligns with venture trends in AI, cybersecurity, robotics, and technologies developed for both military and civilian use cases.

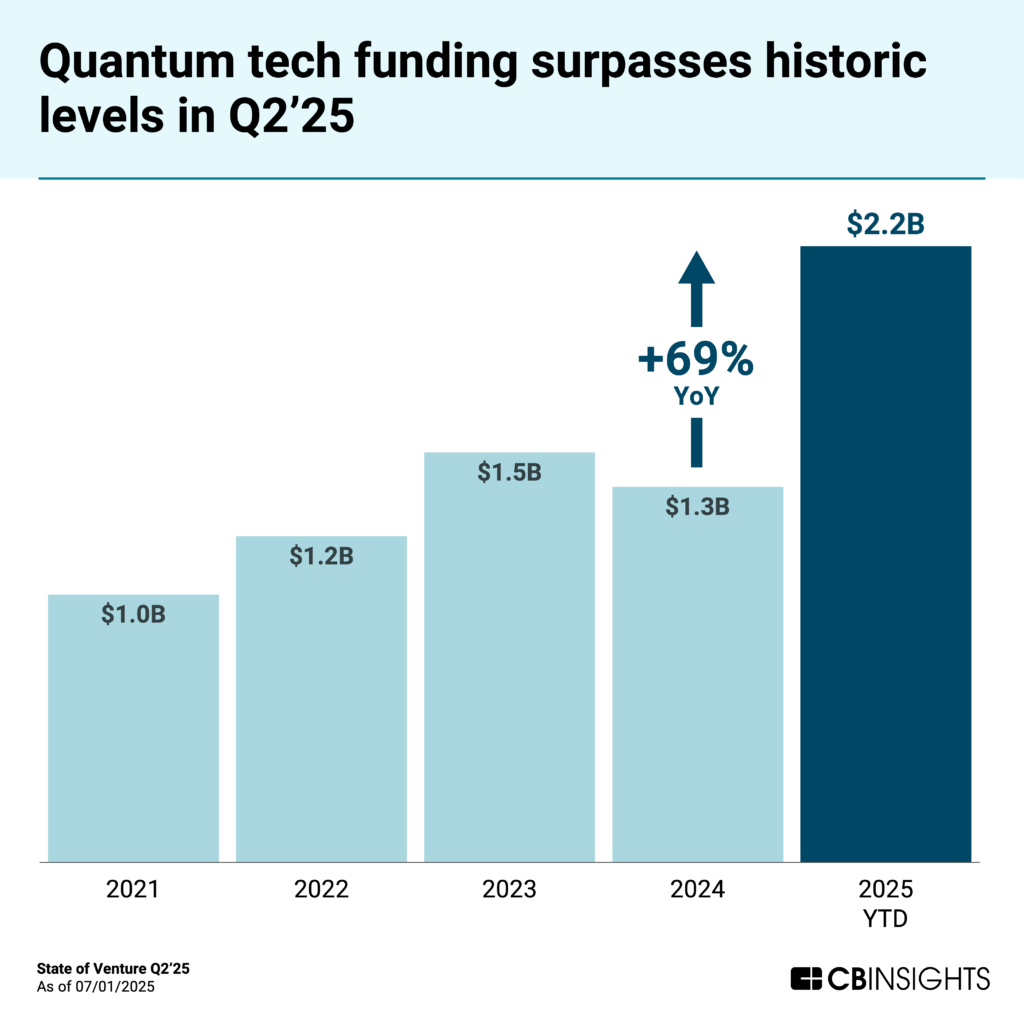

Quantum tech reaches an all-time high, halfway through the year

Quantum tech is attracting significant investor interest, reaching record annual funding levels at $2.2B within the first two quarters of 2025 — an increase of 69% from 2024.

The surge follows major hardware breakthroughs from Google, IBM, and Microsoft, which may drive confidence in leading startups even though the technology still lacks practical applications that outperform classical systems. Industry leaders like Fujitsu and Quantinuum — a subsidiary of Honeywell — expect fault-tolerant quantum computers by 2030 at the earliest.

Massive investments are flowing towards various quantum applications in 2025 so far:

Government support has also increased, with $1.8B in public funding announced globally in 2024. For example, Australia committed $620M to PsiQuantum, while DARPA committed up to $200M in joint funding to assess the feasibility of industrially useful quantum computers.

As quantum technologies move toward commercial viability, the combination of record private investment, substantial government backing, and technical progress positions the industry for significant growth once practical quantum advantage is achieved in commercial applications.

Corporate interest drives a surge in nuclear energy funding

Funding to nuclear energy companies is projected to reach an annual record by the end of 2025 at $5B. Massive energy requirements for AI data centers — with US data center power consumption projected to triple by 2030 — are driving corporate interest in clean baseload power.

![]()

Big tech companies are leading the charge, with investments since 2024 across both small modular reactors (SMRs) and fusion technologies:

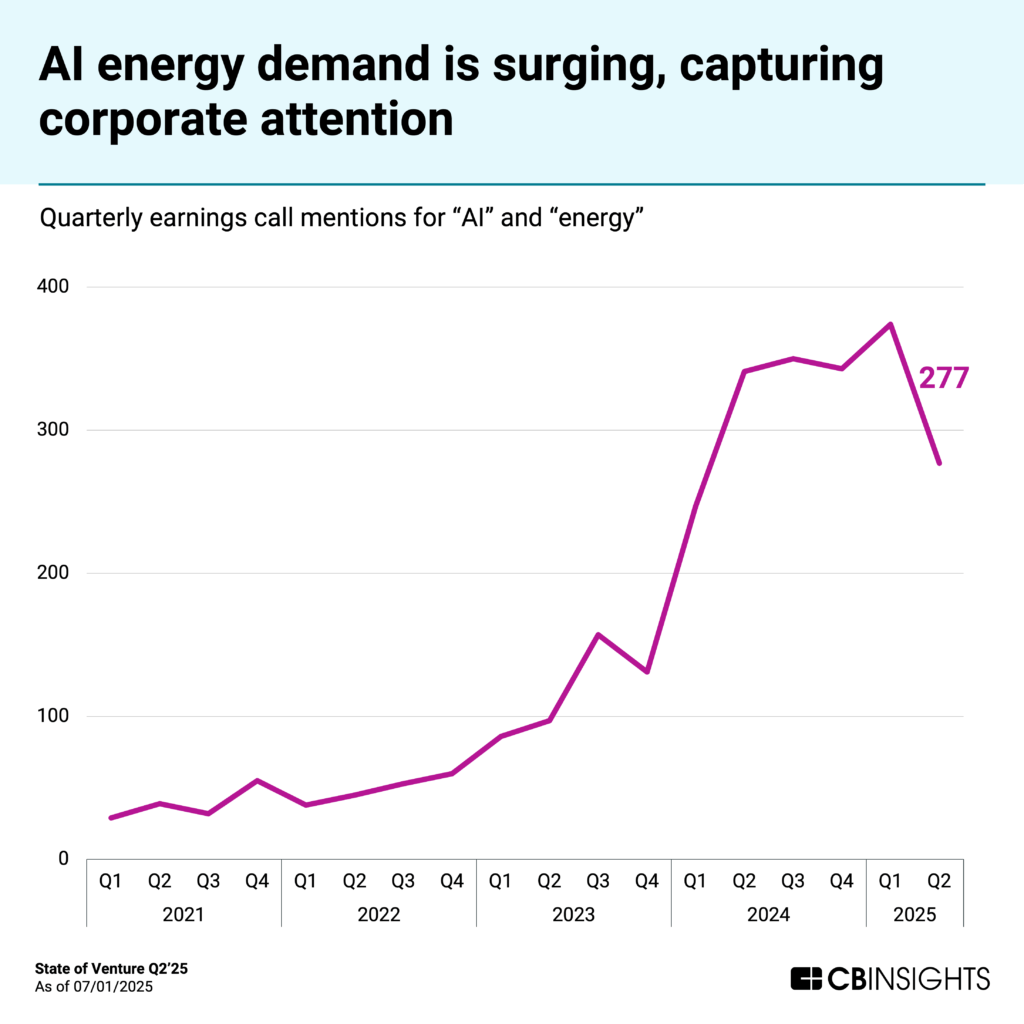

Corporate interest has also skyrocketed, with earnings call mentions hitting record levels as executives grapple with the major power requirements for AI infrastructure.

Current and previous presidential administrations have reduced regulatory red tape for nuclear development, streamlining approval processes. The bipartisan approach creates stable regulatory support for long-term investments and should accelerate sector growth in the coming years.

As AI adoption continues, nuclear provides the only scalable solution for clean baseload power that intermittent renewables cannot match for always-on AI computing infrastructure. The combination of massive corporate demand and supportive regulatory frameworks positions nuclear for explosive growth in the years ahead.

If you aren’t already a client, sign up for a free trial to learn more about our platform.

RELATED RESOURCES FROM CB INSIGHTS:

If you aren’t already a client, sign

up for a free trial to learn more about our platform.